According to Caplight, the 2025 market cycle marked a turning point for late-stage private technology companies. Performance, liquidity, and capital formation all improved materially, with private markets outperforming public benchmarks by a wide margin.

This shift reflects more than cyclical recovery. It signals that private markets, particularly in late-stage venture and growth equity, are evolving into primary venues for price discovery and liquidity.

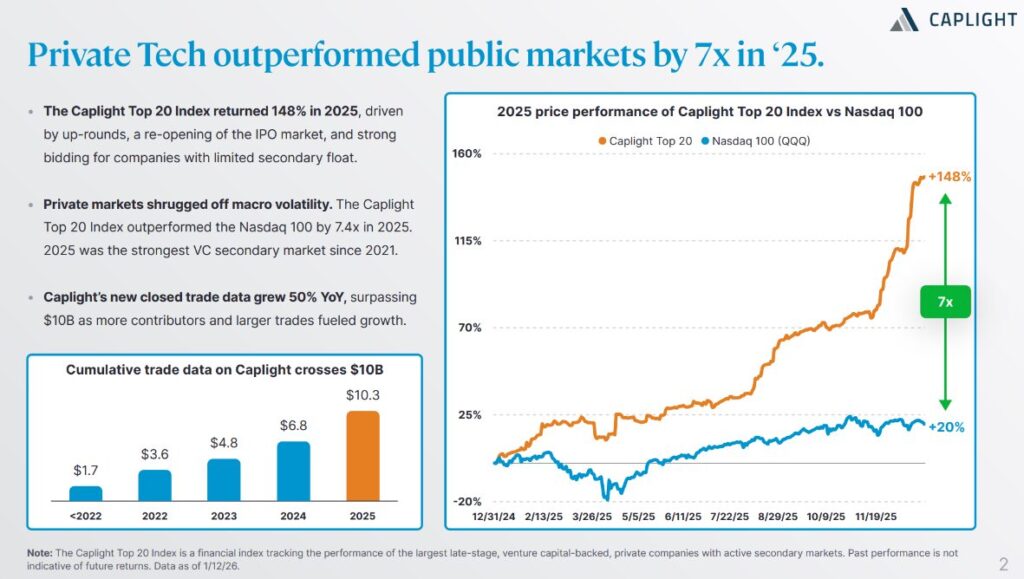

Private Market Outperformance Reflects Structural Demand

The Caplight Top 20 Index delivered a 148% return in 2025, significantly exceeding the Nasdaq 100. At the same time, cumulative secondary trading volume surpassed $10 billion, supported by increased participation and larger transaction sizes.

This divergence highlights several structural dynamics:

- Investor demand for high-quality private assets remains strong

- Limited secondary float continues to support pricing power

- Late-stage private companies are increasingly treated as core portfolio holdings

Private markets are no longer defined by illiquidity. They are functioning as active markets where institutional capital is both deployed and recycled.

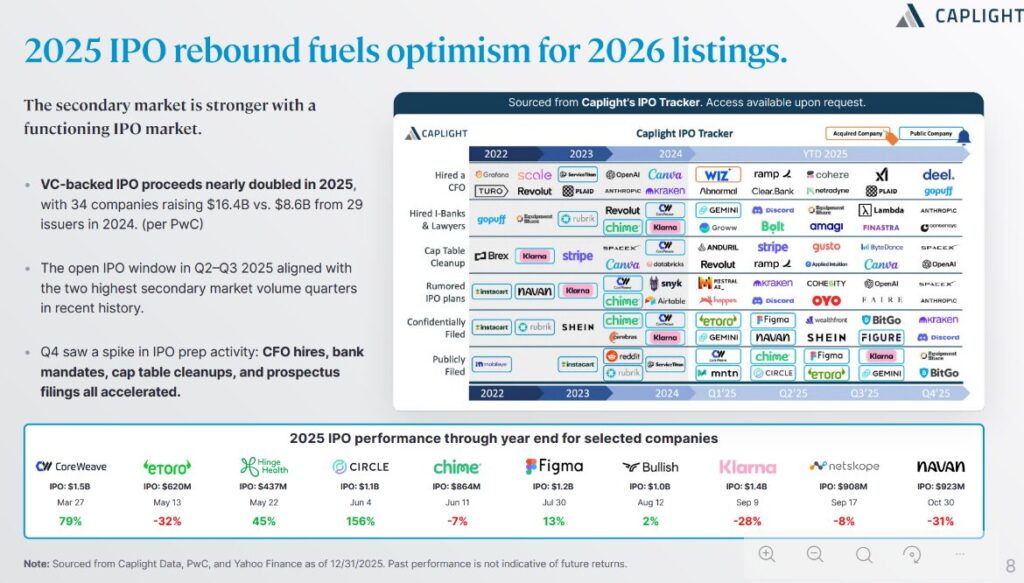

IPO Market Reopening Supports Liquidity but Remains Selective

The reopening of the IPO market in 2025 played a critical role in restoring confidence across venture and growth equity.

Key developments include:

- VC-backed IPO proceeds increased to $16.4 billion

- IPO activity aligned with peak secondary market volume in Q2 and Q3

- Companies accelerated readiness through CFO hiring, bank mandates, and filings

However, post-IPO performance was uneven. While some issuers delivered strong returns, others traded below issue price by year-end. This dispersion reinforces a more disciplined public market environment.

The implication is clear. The IPO window is open, but it is not broadly accessible. Companies must demonstrate durability, scale, and clear paths to profitability.

As a result, secondary markets remain essential in providing liquidity ahead of public listings.

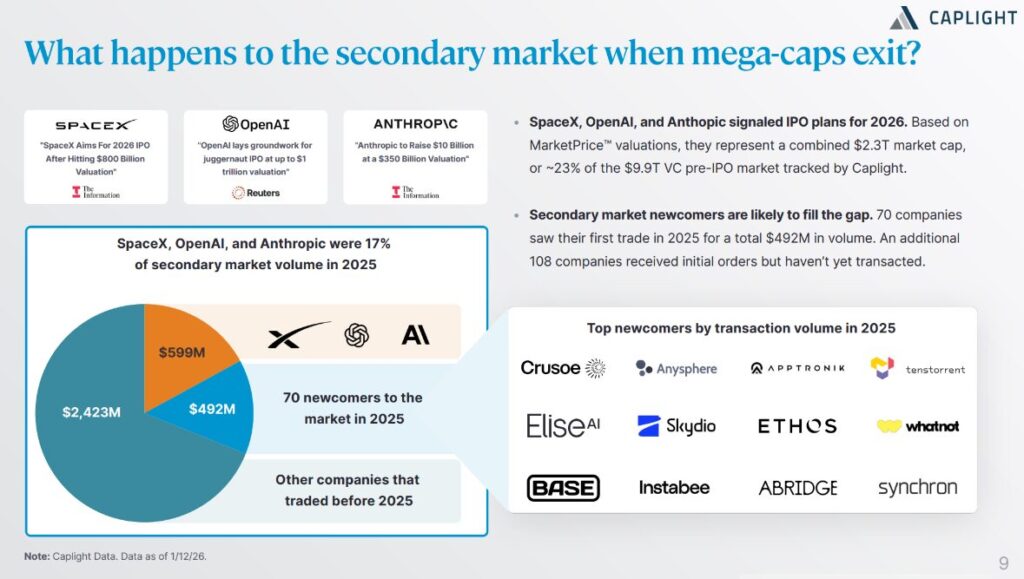

Secondary Markets Expand Beyond Mega-Cap Concentration

Source: Caplight

Large private companies such as SpaceX, OpenAI, and Anthropic represented a meaningful share of secondary market activity in 2025. Combined, they account for approximately $2.3 trillion in value and contributed 17% of trading volume.

Their potential transition to public markets raises an important question regarding future liquidity.

The data suggests the market is already adjusting:

- 70 companies entered the secondary market for the first time in 2025

- Over 100 additional companies have active investor interest but have not yet transacted

- A broader set of companies is beginning to attract meaningful trading volume

This indicates that secondary markets are not dependent on a small group of dominant issuers. Instead, they are expanding into a deeper and more diversified ecosystem.

Liquidity is becoming distributed across a wider range of companies rather than concentrated at the top.

2026 Outlook: Selectivity, Scale, and Sustained Secondary Activity

Looking ahead, the private market environment in 2026 is likely to be defined by three characteristics.

Selectivity in Capital Allocation

Capital will continue to concentrate in companies with strong revenue visibility, defensible positioning, and clear exposure to long-term growth themes such as AI infrastructure.

Continued Growth in Secondary Liquidity

Secondary markets will remain a primary mechanism for liquidity. They provide flexibility for investors and companies, particularly in an environment where IPO timing remains uncertain.

Measured IPO Recovery

The IPO market is expected to remain open but selective. Successful listings will depend on quality rather than momentum. This reinforces the role of private markets as a longer-duration holding environment.

Conclusion

The strong performance of private technology companies in 2025 reflects a broader shift in market structure. Private markets are no longer simply a precursor to public listings. They are increasingly operating as parallel markets with their own liquidity, pricing mechanisms, and investor base.

In 2026, the key drivers of returns will be selectivity, access, and timing. Secondary markets will continue to play a central role in facilitating liquidity and enabling participation in high-quality private companies.

The result is a more mature private market ecosystem, where capital formation and liquidity are less dependent on the public markets than in previous cycles.

Reference: https://www.caplight.com/

Unlock New Opportunities with FNEX Pre-IPO Market

FNEX is a global leader in pre-IPO stock transactions for institutional investors. Our marketplace aggregates bids and offers on late-stage private stocks, with a focus on sectors driving the next generation of value, including artificial intelligence, data infrastructure, and fintech. Institutional participants gain access to exclusive trade data, proprietary pricing metrics, and structured liquidity events designed for precision and privacy.

LEARN MORE ABOUT FNEX PRE-IPO MARKET

Contact FNEX today to buy or sell pre-IPO stocks like Kraken, Space X and OpenAI stocks.

Disclaimer: This material does not constitute tax, legal, insurance or investment advice, nor does it constitute a solicitation or an offer to buy or sell any security or other financial instrument. Securities offered through FNEX Capital, member FINRA, SIPC. The FNEX Pre-IPO Marketplace is intended for use by financial professionals only. Access is restricted to registered investment advisors, broker-dealers, and other qualified institutional investors.