Key Summary

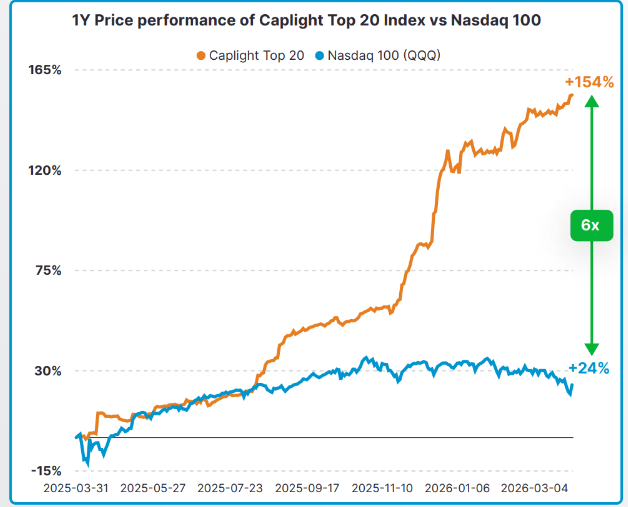

- The Caplight Top 20 Index returned +15.9% in Q1 vs. -5.7% for the Nasdaq 100.

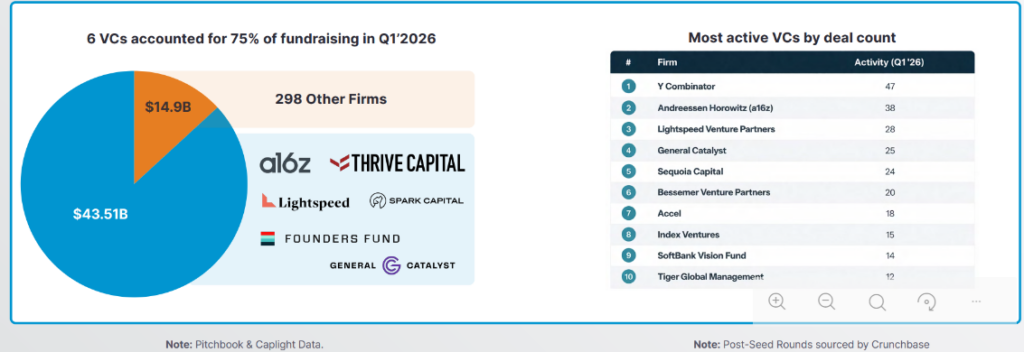

- 6 VC funds raised 75% of all Q1 venture fundraising.

- 5 megadeals absorbed 60% of all primary capital; the top 15 names drove 90% of secondary volume.

- 3 potential IPOs could raise more than the entire 2025 IPO market combined.

- Secondary market sentiment is diverging sharply between Anthropic and OpenAI

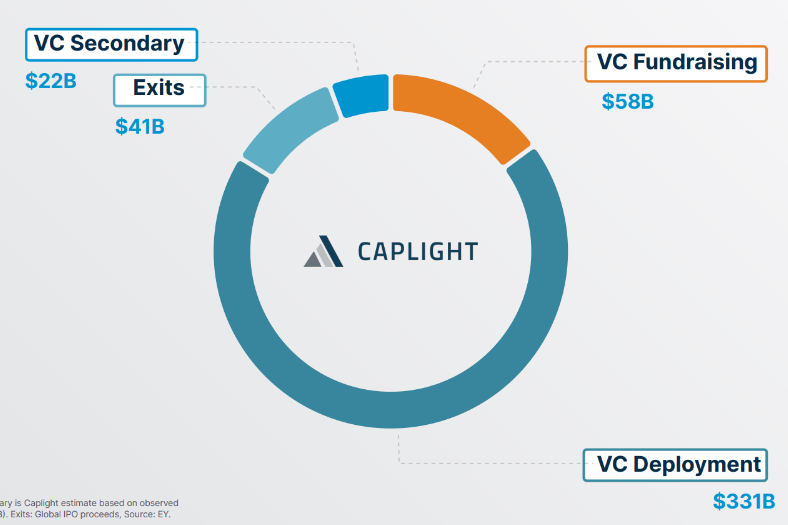

- Caplight now has data on ~45,000 private companies, 34,000 private market investors, and over $300B of secondary market transactional data.

Private tech outperformed, driven by concentrated winners

- The Caplight Top 20 Index returned 15.9% in 1Q’26, outperforming the Nasdaq 100 (−5.7%). Megadeals in AI and defense anchored private valuations while public markets sold off on geopolitical tensions and rate uncertainty.

- Concentration defined Q1. Six firms captured 75% of GP fundraising. Five companies absorbed 60% of primary capital. The top 15 names drove 90% of secondary volume. And three potential IPOs could raise more than the entire 2025 market.

Q1 2026 VC Capital Markets Activity

Q1 was a record quarter for capital deployed, while macro uncer tainty stalled exits

A handful of mega-funds raised all the venture funding

- Six VC managers captured 75% of Q1 venture fundraising, while 298 other funds split the remainder.

- 2025 saw the fewest new VC funds in a decade. Capital isn’t just concentrating at the deal level; the fund managers themselves are consolidating into a winnertake-most structure.

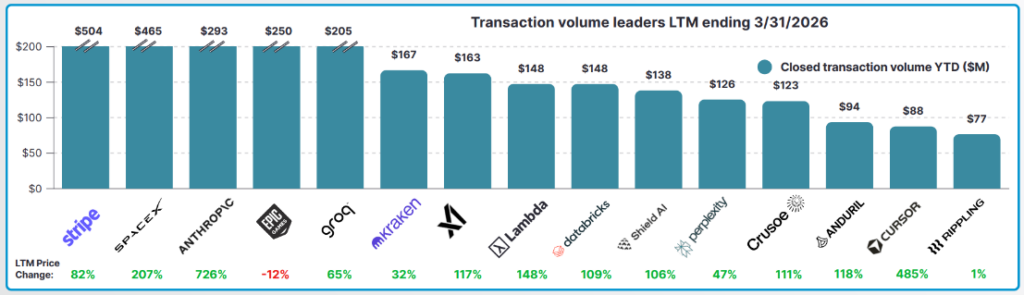

Secondary market trading focused on 15 names

- Market activity remains concentrated, focused on three themes: AI infrastructure, defense tech, and pre-IPO candidates.

- Companies are staying private for longer than ever. The average age of the top 15 most-traded names is ~13 years, compared to a historical median of 5–6 years from first funding to IPO.

- The extended private timeline is driving both volume and concentration. Investors and employees want liquidity, while a growing pool of institutional & retail capital is competing for exposure to these high growth names.

Q1’2026 VC Exits: The bar to go public has never been higher

The most likely IPOs of 2026 generate billions in revenue, compete in the largest TAM’s in history, and need no introduction.

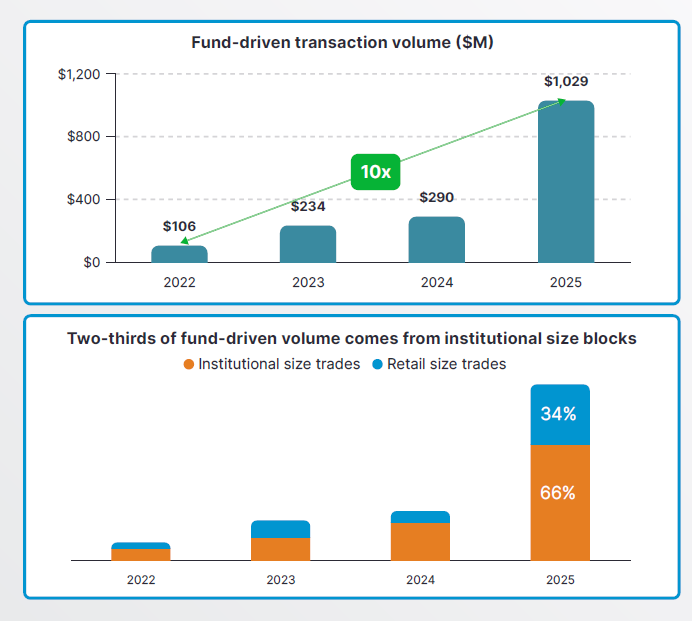

VCs are exiting via secondary market

- Company approved sales of preferred stock reached $1B in 2025, up from $106M in 2022. As the IPO pipeline stays clogged, funds are using secondaries to return capital to LPs.

- Two-thirds of this volume came from institutional sized ($10M+) blocks.

- Fund selling now accounts for 44% of direct trading volume. What was once an employee-driven market is increasingly being shaped by institutional capital flows.

Source: Caplight